This morning we learned that preliminary first quarter GDP came in at 1.6% which was less than the 2.2% expected while PCE inflation readings in the report came in “hotter” than expected. March PCE data will be reported tomorrow. The S&P 500 index had rebounded 2% this week through yesterday. The direction of the market for the remainder of the week will likely depend on how other market behemoths, including Alphabet and Microsoft, report after today’s close. Of course, today’s GDP report and tomorrow’s inflation reading will also be important.

In other economic news, Wednesday’s Durable Goods Orders were reported +2.6% which was better than the +2.0% expected. Combined, these reports suggest the economy continues to perform, but may be slowing. Of course, any additional signs that inflation is not trending toward the Fed’s 2% target will not be welcomed. Tomorrow we will see the Fed’s preferred inflation measurement statistic released, the Personal Consumption Expenditure index.

Regardless of the day-to-day reactions to economic data releases, the market selloff over the past few weeks should not be a big surprise. As Jim pointed out in Monday’s note, the stock market’s strong performance in recent months has been driven by hope that the Fed would soon be cutting rates and excitement surrounding AI. Expectations for Fed rate cuts have been largely diminished and the gains from AI excitement are now baked into valuations.

Almost every CEO now includes a reference to how their company is investing in AI. And yet, so far, the only profits being generated are from those companies selling the AI tools (i.e. chips, software, etc.). Competition and adoption of AI is still in the early innings. Companies investing in AI will have to earn a profit on these investments someday. Monetization of AI for most companies is the next frontier.

If we think about AI like the adoption of the internet, we can expect to see winners emerge over many years. Some companies that will harness the best AI applications may not have even been conceived yet. Other companies may be on the verge of losing their current champion status to competitors that develop better mousetraps. The stock market tries, and often times fails, to value these opportunities and threats accurately in real time.

Take Nvidia for example. Demand for Nvidia’s semiconductor chips currently exceeds production capacity which leads to higher prices and record profit margins. Yet, we don’t know exactly how long this demand imbalance will last. Will competitors will be able to offer something better? If so, when? This is why analysts’ earnings estimates for Nvidia are just educated guesses right now. Currently, estimates for Nvidia’s next year’s earnings range from a low of $21 to a high of $46 per share. For comparison, Home Depot’s EPS estimate range for next year is much tighter, between $15 and $16 per share. Thus, Nvidia’s stock is currently trading for something between 18x and 38x next year’s earnings, depending which estimate ends up being more accurate. In other words, the future earnings of Nvidia are much more speculative to predict than those of Home Depot. This means Nvidia, and other AI focused stocks, will be volatile until the future becomes clearer.

That doesn’t mean one should avoid investing in AI stocks. Rather, investors must accept the inherent uncertainty, volatility, and risk of investing in AI and understand that this is an evolving industry. For those old enough to remember the internet-based stock bubble of the 1990s, consider the early success, but eventual demise, of stocks such as Netscape Navigator, MySpace, AOL, Global Crossing, Commerce-One, etc. Patience, prudence, and deliberate focus on identifying the companies that exhibit characteristics of successful businesses is important when transformational technologies like AI emerge.

For those that want to shoot first, consider the recent example of Cathie Wood’s ARK fund. According to Morningstar, the ARK fund has destroyed more wealth than any other over the previous decade – a cool $14 billion. There is nothing wrong with speculating on disruptive technologies, but speculation is different than investing in proven businesses.

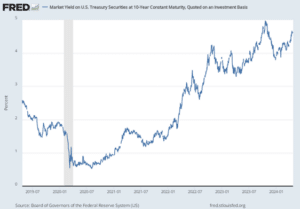

There are lots of AI investment opportunities. But matching opportunities with a valuation disciplined investment approach takes patience. Moreover, interest rates and economic conditions also play a big factor. We have watched as the 10-year US Treasury yield has risen to 4.7%, as of this morning, from 3.9% at year-end and from an historical low of 0.5% during the summer of 2020 (see chart below).

This is a big deal. The 10-year US Treasury bond is viewed as the world’s risk-free asset. All other rates are measured against it. Rising yields make other investments less attractive, particularly stocks with high P/E ratios and associated high growth rates. Yet, up until a few weeks ago, investors seemed not too concerned. If the 10-year US Treasury yield moves close to 5% or higher, companies will have to deliver better than expected earnings growth to maintain current valuations.

It’s hard to watch stock prices go to the moon when momentum takes hold. But history tells us the good times don’t last forever without solid fundamentals supporting the move.

Christopher Gildea 610-260-2235